Let’s be honest—most budgets feel like a diet. You start strong, cutting out all the “bad” spending, but before long, you’re frustrated, tired, and right back where you started. Sound familiar?

That’s because traditional budgeting focuses too much on restriction, not intention.

If you’re a single woman over 40 managing your finances solo, you don’t need a one-size-fits-all budget—you need a spending plan that works for your real life.

That’s where intentional spending comes in.

Giving your money a job that matches your values. Not just tracking dollars, but choosing where they go on purpose.

💡 This post is part of the Smart Money Management Series — your step-by-step guide to financial confidence for independent women. Visit the Solo Money Hub » to see all 6 parts and grab your free Starter Kit!

Just a Heads Up! 🌟 This post may contain affiliate links, which means I might earn a small commission (at no extra cost to you) if you make a purchase through one of these links. As an Amazon Associate, I earn from qualifying purchases. But don’t worry—I only recommend products and services I personally use, love, or believe can genuinely benefit you. Your support helps keep this blog going—thank you! 💖

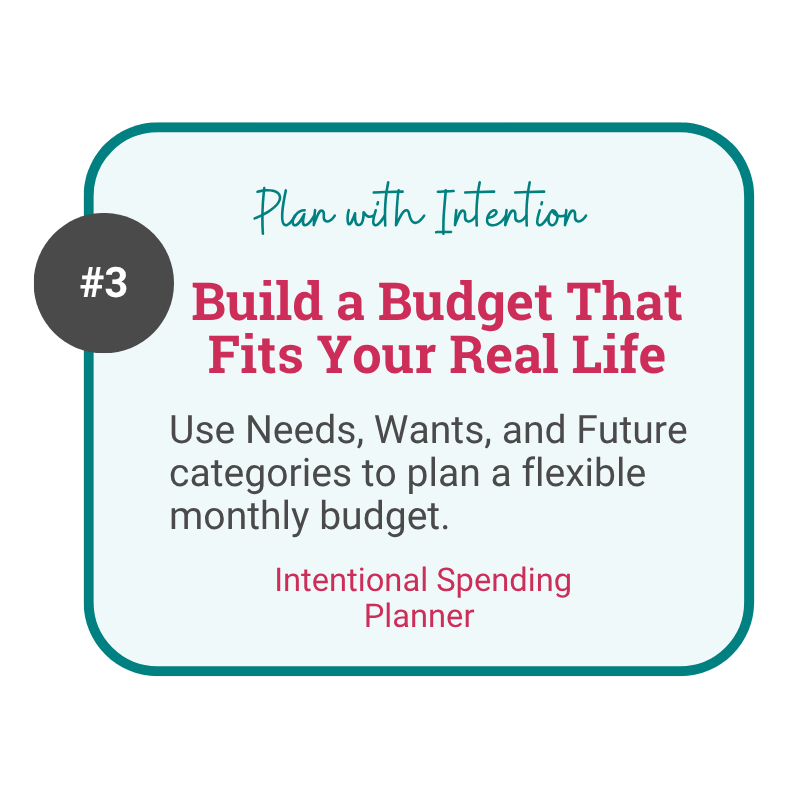

This step uses my simple Needs, Wants, and Future method to build a plan that’s flexible, realistic, and actually sustainable. This method keeps you financially secure while still allowing you to enjoy life.

Why Most Budgets Fail (and How to Fix That)

Before we build your spending plan, let’s address why budgeting has felt so hard in the past.

The old-school budget approach:

🙅♂️Count every penny with no flexibility.

🙅🏽Makes you feel guilty for every “unnecessary” purchase.

🙅♀️Ignores your actual lifestyle and what brings you joy.

An intentional spending plan:

👍🏻 Gives you freedom within a structure that works for you.

👍🏽 Helps you spend on things that bring value while getting rid of what doesn’t.

👍🏿 Accounts for your future, not just your present.

If you’ve ever tried to budget and given up, it’s not because you lack discipline—it’s because the method you were using didn’t fit your life.

That’s why an intentional spending plan is different—it’s not about restricting yourself or obsessing over every dollar. It’s about aligning your money with what actually matters to you, so you can feel financially secure without feeling deprived.

💡 Fact: According to Debt.com, 27% of people avoid budgeting because it’s too time-consuming, 20% say it makes them feel guilty, and 29% believe they don’t earn enough to bother.

How to Build an Intentional Spending Plan

Instead of a strict budget, we’re going to structure your money into three simple buckets: Needs, Wants, and Future. That’s it.

You’re not trying to be perfect. You’re creating a plan that works with your real life—not someone else’s idea of how you should spend.

Let’s walk through each one:

1️⃣ Needs: The Essentials (50-60%)

These are the must-haves—the things you need to keep you safe, healthy, and stable. The things your life depends on, like:

❇️ Rent/Mortgage

✳️ Groceries

❇️ Utilities

✳️ Health Insurance

❇️ Transportation

💡 Tip: Many people overestimate what’s truly a “need.” Before assuming you must spend a certain amount, ask yourself: “Is there a cheaper or simpler way to reduce this cost?”

2️⃣ Wants: The Joyful Extras (20-30%)

This is where things usually fall apart—not because you’re spending too much, but because you feel guilty about spending at all.

Wants aren’t bad. They’re part of living a good life. The key is making sure you’re spending with intention—not just out of habit or to avoid stress.

Think about what actually brings you joy versus what just fills time. That’s where your “wants” budget should go. Here are some examples:

☕ Eating out & coffee runs

✈️ Travel & entertainment

🛀 Hobbies & self-care

🎧 Subscription services

💡 Fact: A 2023 NerdWallet survey found that 83% of Americans say they overspend, and 84% of those who budget say they exceed their monthly budget.

3️⃣ Future: Security & Growth (10-20%)

This bucket is often the most neglected, especially for women managing money alone. But it’s the one that creates freedom.

Want to come back to this later?

Even small amounts toward savings, debt payoff, or long-term goals matter. This is your cushion, your backup plan, your future peace of mind.

🚨 Emergency Fund

💰 Retirement Savings

📊 Investments

⛓ Debt Payoff

💡 Fact: A Bankrate survey found that 57% of Americans can’t cover a $1,000 emergency expense, forcing many into debt when unexpected costs arise. Also, about 33% have more credit card debt than emergency savings.

How to Put This Plan into Action

Understanding where your money should go is one thing—putting it into action is where the magic happens. You don’t need to map out your entire future in one night. Start simple, and build from there.

Track Your Current Spending

Before you make changes, just see where your money is actually going.

Use a notebook, your phone’s notes app, or even voice memos if that’s easier. Jot down every expense for a week or two—without trying to fix anything yet.

This isn’t about judgment. It’s about getting honest with yourself so you have a solid starting point.

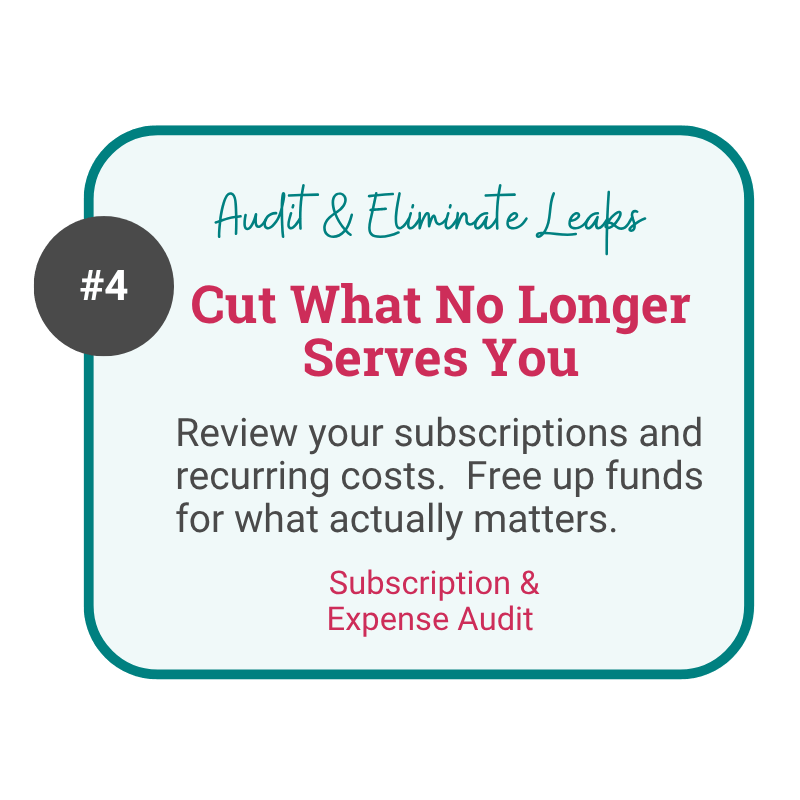

Compare Your Current Spending to the Needs, Wants & Future Framework

Once you’ve tracked a bit, hold your numbers up against your new mindset:

- Are your “needs” really needs—or could they be trimmed?

- Are your “wants” bringing joy or just filling time?

- Are you investing anything in your future self?

This is your moment to adjust—not restrict. Tiny changes now can make a huge difference later.

Real-Life Shift: From Surviving to Spending with Intention

You don’t need a total life overhaul to start spending more intentionally. Sometimes it’s just about noticing where your money actually goes and asking, “Does this still work for me?”

A while back, I realized I was spending way more on takeout and impulse buys than I thought. It wasn’t that I loved those things—it was just easy. They became my default during stressful weeks.

But once I tracked it all and compared it to the Needs, Wants & Future framework, it clicked.

I didn’t cut everything out. I just shifted things around:

- Kept a little takeout budget, but used the rest to grow my emergency fund.

- Paused the random spending and started a “fun fund” for travel.

- Finally set up those auto-transfers to retirement that I’d been putting off forever.

It wasn’t perfect. It didn’t happen all at once. But it gave me momentum—and that was everything.

Pin This Post:

Final Thoughts: Progress > Perfection

You don’t need to budget like a robot. You just need a simple system that helps you stay aware and adjust as life happens.

Here’s a little nudge:

📌 Track where your money’s going.

📌 Compare it to your needs, wants, and future goals.

📌 Make one small change this week—even if it’s just canceling a subscription or setting up a tiny savings transfer.

That’s how you build better money habits—one tweak at a time.

🧭 Next Up: Part 4 – Build a Financial Safety Net on One Income »

Want a little more help with your money?

Explore Smart Solo Money for simple ways to organize your finances and reduce money-related stress.

PIM Community Question:

What’s one area of your budget you’d like to be more intentional about? Tell me below—I’d love to hear your thoughts.